Australian mine explosives major Orica says technological advances are reshaping the mining landscape. The A$8.35 billion (US$5.3 billion) company is one of two types of supplier set to fight for control of that landscape over the next decade.

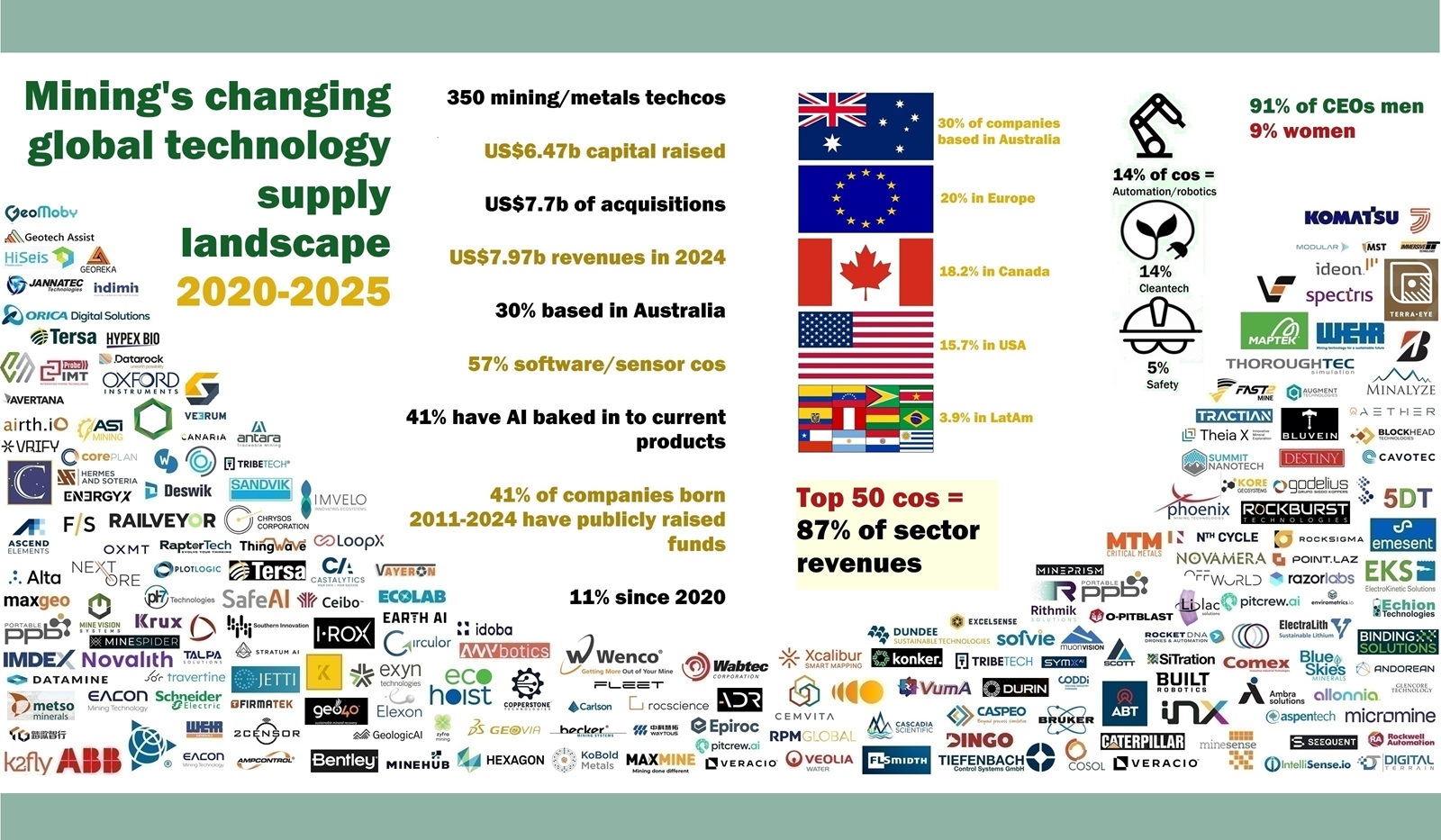

An InvestMETS.com deep dive into the world’s 2025 mining and metals technology pool – 350 companies behind US$14.2 billion of financing and M&A in the past five years – underscores the market bifurcation.

Orica is among the large traditional, or incumbent, suppliers that currently control nearly 90% of the world’s mining and metals-linked technology sales. The market is ruled today by software, sensors, automation and control systems, various types of clean processing tech, and advanced safety products. A swarm of potential disruptors, most born in the past 15 years, are seeking to upend mining’s conventions and the entrenched positions of traditional suppliers.

History says they’ll slide into mining’s seemingly bottomless valley of death. But the more recent past indicates exponential rates of technological change coupled with escalating geopolitical upheaval and pressure on miners to expand production while meeting higher environmental and social standards is creating a perfect storm for profound shifts in the technologies delivering primary and secondary metal flows.

Many of the world’s largest suppliers of equipment and products to mine owners overhauled traditional business models between 1995 and 2010 by massively upscaling aftermarket activities and growing services revenues. Now they are reimagining themselves as technology companies, replicating patterns in the much bigger international oil and gas market that go back decades.

Komatsu, Hitachi Construction Equipment, ABB, Schneider Electric, Epiroc (ex-Atlas Copco), Sandvik and Orica have been major buyers of technology firms over the past decade, along with tech consolidators such as Constellation Software, Hexagon and Bentley Systems. Private equity groups have also been active.

The level of acquisition activity in the sector grew to unprecedented levels 3-4 years ago and has remained at elevated levels. Epiroc’s reported interest in Australia’s Micromine, which may now have a A$1 billion price tag, comes on the back of US-based Wabtec Corporation’s recent US$1.78 billion purchase of Evident Scientific’s inspection technologies arm. There are other potential billion-dollar deals in the pipeline.

Digital and automation technologies, and firms, have been the focus of most of the 116 significant mining/metals tech acquisitions, worth at least US$7.7 billion, between 2020 and now. These deals have underpinned the growth of technology divisions under some of the industry’s biggest incumbent suppliers.

However, 90% of the $6.47 billion of growth capital raised by mining/metals tech entities in the past five years has gone to 146 firms born between 2011 and 2024. All up, more than half the 350 tech firms were formed in this period.

This sector epoch has seen a significant volume of funding flow into the urban mining tech landscape, rather than the primary mining market, and it has also seen a raft of more sustainable exploration, mining, mineral processing, energy and water technologies win investor backing.

The period has also seen the conception and rapid rise of Chinese mining tech companies, including mining automation firms that have raised more than $350 million of equity funding and, unlike their Western counterparts, have achieved fast, large-scale deployment at domestic mines. At current adoption rates and given the ongoing expansion of China’s state-backed miners offshore, this is set to become a pivotal point of difference between Chinese and Western start-ups in the space. The global autonomous mining truck market could be worth $12.5 billion by 2035, according to Allied Market Research.

“There needs to be an external catalyst to drive change – a Tesla for mining equipment,” says a veteran Australian mining tech leader. “There is huge opportunity for new entrants.”

Western investors have meanwhile placed sizeable bets on new mineral extraction and mine-waste valorisation approaches that may be key to unlocking trillions of dollars’ worth of resources; segments of a lithium-ion battery value chain Canada’s Summit Nanotech says will provide more than $400 billion of revenue opportunities by 2030; and urban metal recovery and recycling technologies targeting markets US-based Sortera believes are already worth more than $1 trillion.

Disruption is the mantra of companies such as Fleet Space Technologies (terrestrial mineral exploration); Chrysos Corporation (mineral sample analysis); Jetti Resources (low-grade sulphide copper recovery); and Hypex Bio (ammonium nitrate explosives). And many others.

Canada’s Tersa Earth says $20 billion worth of metals “are lost in tailings ponds” every year in North America alone. “Without improved mining remediation technology it’s estimated that over 75 trillion litres of acid rock drainage will be produced globally by 2040.” VerAI, a US company, claims it can generate mineral targets 20-times faster and cheaper than traditional methods.

“The decline in high-quality, easily accessible deposits intersects with growing demands on the industry to ramp up production,” RCF Innovation principals Andrew Jessett and Charles Gillies wrote this month.

“Between now and 2050 the energy transition may require as much as 6.5 billion tonnes of end-use materials. It is estimated that 95% will be steel, copper and aluminium with the rest comprising critical minerals such as lithium, cobalt, zinc, graphite, nickel or rare earths.

“Geopolitical concerns are adding to production pressures as governments are realising the danger of relying on rival foreign powers for critical minerals. The mining industry is also under considerable pressure to address environmental, social, and governance concerns including local community impact, waste and tailings management, worker safety and mine site carbon emissions.

“Labor scarcity is driving further change. According to the Society for Mining, Metallurgy & Exploratio, more than half the mining workforce in the US, about 221,000 workers, is expected to retire by 2029. And despite the fact that mining is projected to consistently add thousands of stable, high-paying jobs over each of the next 20 years the industry is struggling to attract and retain the workers it needs.

“Industry leaders are acutely aware that tomorrow’s mines must be substantially different in order to keep pace with this conflicting set of demands.”

Jessett and Gillies claim mining has “always been a leader” in transformation and innovation and they point to early adoption of autonomous heavy vehicles as proof the industry can adapt. Wider adoption of autonomous machinery, though, has been slow. Not everyone agrees with the idea that miners are leaders in the innovation stakes.

“The fundamental problem is the fact that innovation is not playing a role in the way ore is produced,” Doug Morrison, CEO of the Centre for Excellence in Mining Innovation in Canada, said at this year’s Future Minerals Forum in Riyadh, Saudi Arabia.

“I was involved in my early career in the early 80s when we made the transition from very manually intensive, selective mining methods with very small handheld drills and we changed over to the equipment that we have now: large rubber-tyred machines, LHDs, trucks, etc. That transition was made by 1985.

“That technology platform has not changed in the last 40 years.

“There is no other sector in the economy that is using a technology platform that is 40 years old.

“The waste management practices of the industry have not changed one iota in 40 years.

“No other industry could get away with this in the modern era and this is the crunch that we’re all confronting now. We have to change our production practices and we have to change our waste management practices.

“We have to move away from the idea of using 1%, 2% or 3% of the resource and leaving the other 97%; especially leaving it in a highly toxic pond of waste which is no longer desirable to even some of the poorest communities in the world.”

*InvestMETS.com’s full report on the changing global mining and metals technology supply landscape, including a listing of the top 50 tech companies in the sector, appears in the March edition of The Mining Tech Report.